The stock was suspended for more than two months, but it was closed on the day of the resumption of trading. In the evening, the company issued an urgent announcement that the actual controller and its related party pledge stocks had nearly closed the line and had to suspend trading again.

This is a very eye-popping scene that happened recently on the A-share listed company of the cross-border education.

On February 6, Qinshang announced that it will suspend trading for major events until April 25. However, the market closed down on the day of the resumption of trading, the company's actual controller Li Xuliang and his related person Li Shuxian part of the pledged stock is close to the liquidation line. Therefore, Qinshang shares announced that the company's stock will be suspended again from the next day and seek ways to solve the risk.

The reason for the downside of Qinshang shares and the risk of closing the equity pledge may be related to the short-term performance of “big face changeâ€, loss of 427 million yuan, and mergers and acquisitions of Chengda’s investment, indirect merger and acquisition of Chengdu Qizhong Experimental Middle School.

Looking back at the 2016 A-share market, a number of listed companies began to cross-border M&A education assets, and Qinshang shares were no exception. If the completion of the acquisition of Guangzhou Longwen Education is the beginning of the transformation of Qinshang Shares and the implementation of the “LED+Education†dual main business model, through the statistics of Blue Whale Education, this logistics stock announced a total of six educational assets mergers and acquisitions, involving the amount About 4 billion yuan. Such a fierce acquisition is particularly prominent among listed companies in A-share cross-border education. However, this time Guangzhou Longwen failed to complete the promised performance, Qinshang shares received the discussion of the relevant "terminating agreement" of Chengdu's investment, which seems to cast a shadow over its "LED + education" dual main business development model.

Why did Guangzhou Longwen Education fail to complete its promised performance after being acquired by Qinqin Shares? What are the reasons for the loss of performance, restructuring, and risk-taking diligence? Previously, Blue Whale Education had counted 65 mergers and acquisitions in the capital market in 2016. There are many high-performance promises and high-value cross-border mergers and acquisitions cases. The impairment of goodwill and performance losses of Qinshang Shares may be the initial performance of “sequelâ€.

2 billion yuan cross-border acquisitions in exchange for performance?

Diligence shares may have a worse-than-expected loss due to performance failures. On April 21, Qinshang Co., Ltd. released its 2016 annual report. The net profit attributable to shareholders of listed companies was a loss of 427 million yuan, a year-on-year decrease of 2160.66%. However, the revised performance report of Qinqin shares showed a net profit loss of 396 million yuan. For the huge losses, Qinshang explained that the performance of Guangzhou Longwen Education “has not reached expectationsâ€.

For a cross-border merger with a price of 2 billion yuan and a premium of 30 times, the acquisition has created a goodwill of 2 billion yuan in the company's balance sheet; and "not up to expectations" directly caused a loss of goodwill of 420 million yuan.

Looking back on the acquisition, in early 2016, Qinshang announced that it intends to purchase a stock and pay cash for a total of 2 billion yuan to purchase Guangzhou Longwen Education, which is in a state of negative equity. Such a high-value acquisition in the state of undervalued assets immediately attracted everyone's attention, including the Shenzhen Stock Exchange. In the face of the Shenzhen Stock Exchange's inquiries, Qinshang shares said that the K12 counseling industry has good prospects for development, and Guangzhou Longwen has the characteristics of light assets and high cash flow.

After the semi-annual release of the reorganization and restructuring of Qinqin, the CSRC was “conditionally passedâ€, and the speed exceeded the general expectations of the industry. At the same time as the completion of the acquisition, the original shareholders of the target promised a net profit after tax of not less than 564 million yuan realized in 2015-2018. Blue Whale Education noted that Qinshang had predicted that Guangzhou Longwen achieved a net profit of RMB 100.3 million in 2016. However, the actual net profit was RMB 66.426 million, and only 66.19% of the promised performance was achieved.

Why did Guangzhou Longwen Education fail to fulfill its performance commitment after the completion of the merger?

In this regard, Qinshang shares explained that Guangzhou Longwen eliminated the teaching points with backward operating conditions, and standardized software and hardware transformation of the superior teaching points to improve the unit price. However, due to fierce market competition, the increase in the unit price of the class does not compensate for the decrease in the number of teaching points. Therefore, the overall revenue of 2016 has declined to a certain extent. In addition, after the integration of Longwen Education into the listed company, there is still a certain running-in process. It is unable to give full play to the potential of its management staff and sales team in the peak season of the tutoring industry. The business development and outlet layout are lagging behind, resulting in income. Sliding down.

Why is it not clear whether Guangzhou Longwen has completed the income expectation? Qindi said that due to the large number of Guangzhou Longwen national business outlets, the previous performance appraisal and the determination of future business plans are not comprehensive, and the decision-making basis is incomplete and decision-making. The process was unscientific and failed to find timely signs of impairment in Guangzhou Longwen's goodwill.

In addition, Blue Whale Education noted that Qinshang shares issued a performance amendment announcement on April 14 and announced that Vice President and Secretary-General Hu Shaoan had resigned for personal reasons. However, on March 10, Qinshang Co., Ltd. passed the review on the appointment of Hu Shaoan. For the relevant secretaries of the Secretary.

In response to the company’s performance of “Diversity Change†and the resignation of former Secretary-General, Blue Whale Education asked about Qinqin’s shares. As of press time, Qinshang shares have not yet responded.

Where does the gambling education dual main business model go?

Why did Qinshang Group acquire Guangzhou Longwen in 2016? This may be related to the fierce competition and slowdown in its original semiconductor industry. A person familiar with the matter once told the Blue Whale Education that the LED industry has not much room for imagination, the threshold is very low, the market competition is fierce, and the gross profit continues to decline. Almost all of the listed LED companies are undergoing transformation or doing dual business. Moreover, the current market valuation of education is still very high, and the acquisition of the education industry can be recognized by the capital market.

Qinshang shares in the 2015 annual report, the acquisition of educational assets into the educational industry, in order to cope with the decline in its operating income, improve its sustainable profitability, and achieve value enhancement and transformation. Coincidentally, another LED manufacturer, Changfang Group, also successively acquired the offline kindergartens and opened educational subsidiaries in late 2016 to seek the development of “LED+Educationâ€.

Li Xuliang, the actual controller of Qinshang, said at the reception agency that the transition education is looking for new profit growth points to give back to all shareholders. An analyst told Blue Whale Education that Qinshang shares increased the purchase of Guangzhou Longwen Education by 1.8 billion yuan. Li Xuliang and his sister Li Shuxian spent 972 million yuan to participate in the subscription. This shows that Li Xuliang is confident in transition education. of.

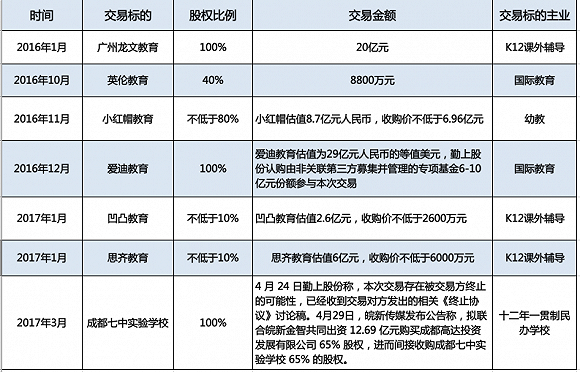

After completing the merger and acquisition of Guangzhou Longwen Education, Qinshang shares have been non-stop and attacked everywhere. So far, six education-related mergers and acquisitions have been announced.

Throughout the mergers and acquisitions of Qinshang shares, the main business of the subject matter involves early childhood education, K12 tutoring, international education and private schools. Qinshang shares announced in August 2016 that the company has established a K12+3 (ie 3-18 years old) strategy, which clarifies the layout of the education industry chain from early childhood education to K12 education to international schools.

However, the house leaked to the night rain. On April 24, Qinshang shares announced that it had received a discussion draft on the relevant “Termination Agreement†issued by Chengdu Gunda Investment Development Co., Ltd., when Qinshang said that it would “really negotiate with the counterparty according to law. We will strive to promote relevant solutions in the existing negotiation and negotiation results and actively protect the company's various rights and interests." Only after six days, Fuxin Media announced that it plans to jointly invest RMB 1.269 billion in Fuxin Jinzhi to purchase 65% of Chengdu Gaoda Investment, and then receive a 65% stake in Chengdu Qizhong Experimental School. Some people believe that Fuxin Media has issued a proposed acquisition announcement this time, basically announcing the divestment of the company.

On the one hand, the high-yield high-performance promised acquisition of the education target performance "not up to expectations", the other side and Chengdu Qizhong realized the school's impending exit, how can Qinshang shares be able to achieve their director, financial director Deng Jun Hongzi responded at the performance briefing "Continue to adhere to the development of LED and education dual main business"? How can a listed company with cross-border education expand its education business?

"The quality of the education target will affect the development of the education business after the listed company's merger and acquisition. The newly listed listed company may wish to know what the reputation of this institution or school is in the industry before the merger, if the target is resold a lot. There are no results in the year, so it may need to be carefully considered." An industry insider gave the above suggestions.

A securities analyst told Blue Whale Education that the dual-main business model may be just a transitional approach for listed companies. Many companies will gradually divest or split their original businesses after a period of development. Great interest. Tilting to the second main business is a trend.

People in the education industry told Blue Whale Education that for listed companies that cross the border, they should do a good job in pre-research and always pay attention to the development of the new main business before learning the subject of education and entering the education field. And the introduction of talent is crucial.

Blue Whale Education combed the company's 2016 annual report and found that among the directors, supervisors and senior management personnel of Qinshang, apart from the independent director Wang Zhiqiang, no one has experience in the education industry.

Listed company "double high" mergers and acquisitions sequelae?

In recent years, affected by the overall economic environment, many listed companies are facing the dilemma of the downward pressure of the main industry and the increasingly obvious ceiling effect. Especially the traditional manufacturing industry encounters many bottlenecks in the process of development, so it is necessary to find new profit growth points. The top priority for these listed companies.

In Zhang Hui, director and executive vice president of Huiguan, the listed companies are looking for new profit growth points in the cross-border nature. In addition, the valuation center of the entire capital market is declining, resulting in many companies needing new assets or concepts. To maintain the existing valuation system and promote the market value to continue to grow.

Under various circumstances, the counter-cyclical education industry has become one of the best choices for cross-border companies. In addition, influenced by the policy and the expected dividends of the demographic dividend, the education industry has a huge upside, known as the “sunrise industryâ€. Therefore, it can be seen that in the past two or three years, a number of listed companies have cross-border M&A education assets and cut into the education industry, among which there are many high-value, high-performance commitments.

"Listed companies are willing to accept high-performance promises to bring high valuations, not to rule out to raise the stock price and profit from it." An analyst told Blue Whale Education.

At the beginning of 2015, Quantong Education acquired a high premium and entered the Jijiao Network and Xi'an Xiyue. The premiums were 9.4 times and 18.5 times respectively. However, the network has not completed its 2015 performance commitment. An education industry investor once told the Blue Whale Education, "I am very distressed and all-pass, and it is expected to have a negative effect on the education sector."

In September 2016, San Aifu plans to acquire two educational targets, and the estimated assets of the two targets have increased by 1805.1% and 1274.9% respectively. Ovia, one of the acquisition targets, had a net profit of less than 35 million in 2014. Its shareholders have promised that the net profit after deduction in the next three years will not be less than 110 million yuan. Immediately after the reorganization plan was thrown, the Shanghai Stock Exchange was asked to ask San Aifu to explain the reasons for the high premium purchase and the achievement of the performance commitment. This pile has acquired mud cows into the sea.

Huang Bo, chairman of Hongcheng Education, told Blue Whale Education that “if the target does not meet expectations, the goodwill of the listed company will be greatly impaired, and the goodwill is the difference between the valuation and the fair value of the acquired company. In the next two to three years In the case, we will see that the profits of many listed companies that have made a large number of acquisitions will be affected by the impairment, and the impact on net profit will be very large. In recent years, the A-share market has carried out too many educational target mergers and acquisitions, the next two years, the problem It may appear slowly."

In the face of the trend of cross-border mergers and acquisitions, Wu Guanxiong said, “Listing companies must first rationally consider the growth of their performance in the acquisition of educational assets; secondly, whether the target and the acquirer can be integrated. In the merger, the educational institutions are special. It is a traditional educational institution that does not have such a high growth rate in most cases. It is a long-cycle industry."

When “Double High†acquired the education target, it is not uncommon for listed companies to implement the dual main business model. After the short-term stock price is popular, how can listed companies integrate the original main business and the education industry to achieve “cooperative development� Manpower and material resources How to allocate financial resources? How should listed companies manage high-value, high-performance, promised mergers and acquisitions may bring "sequel"? These are old-fashioned questions, but there is still no question.

UKK Power Distribution Box- 95% contact- Flame retardant:UL94 V0- Nickel-plated copper conductor:copper cable or aluminum cable- The maximum withstand short-circuitcurrent can reach 100KA- Comply with ROHS,CE- Flexible busbars can be directly ibserted into the connection(UKK 500A)- Flexible busbars can be inserted and connectedwith flat connectos(UKK 250A&UKK 400A)

Power Distribution Terminal Box , Brass busbar Distribution Terminal blocks with removable cover A Distribution block is an economical and convenient way of distributing an electrical circuit from a single input source, to several devices in the branch circuit. Thus reducing the total number of wires in your electrical panel and saving you time and money. The exclusive compact and modular design of our distribution blocks.

Electric Supplies Box,Distribution Switchgear,Distribution Circuit Breaker Box,Plastic Power Distribution Box

Wonke Electric CO.,Ltd. , https://www.wkdq-electric.com