There are more and more electronic devices and systems in the car, and they are also the driving force for automotive functional innovation.

This article refers to the address: http://

Automotive manufacturers are increasingly using electronic systems and semiconductor integrated circuits for a variety of automotive applications, including driver information and communications, in-car entertainment electronics, powertrain and body control electronics, and automotive safety and comfort devices.

The global sales of 700 million vehicles per year provide a huge market opportunity for automotive electronics. Car sales in Western Europe alone reached approximately 250 million vehicles. According to market research firm Research & Markets (Research and Markets), by 2010, the proportion of electrical and electronic components used in automobiles to total vehicle costs will increase from the current 25% to 40%. Electrical integration in automobiles Half of the electronic components and semiconductor components are semiconductor integrated circuits. With market value reaching 123 million euros ($180 million) in 2011 and an average annual growth rate of 6% to 9%, automotive electronics will become one of the major sub-markets in the electronics market.

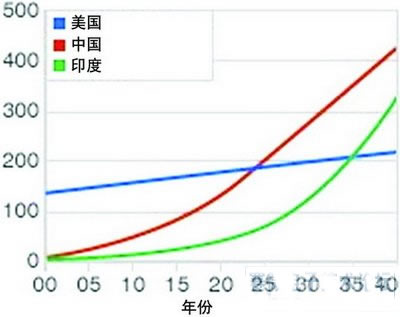

Figure 1 Global car ownership forecast

Source: Goldman Sache Economist

This growth rate is in stark contrast to the growth rate of global automobile production. The average annual growth rate of global automobile production during the forecast period is about 3%. Therefore, in terms of sales revenue, the automotive electronics market is growing at a much faster rate than the automotive market. This shows the general trend of increasing electron density and complexity in the enterprise. According to the German ZVEI (German Electric and Electronics Industry Association) organization, the global automotive microelectronics market will grow by 11.9%. By 2011, the global automotive microelectronics market sales revenue will increase from $19.1 billion in 2006 to $33.5 billion.

Automotive electronics has become one of the major differentiation standards in the automotive market. In the automotive market, where profits are significantly reduced, sales and production growth are declining, competition is becoming more intense, and cars are becoming more commoditized, automotive electronics will add value to cars, especially in Western Europe.

An important driver of the automotive market is regulations that require management to increase safety and reduce vehicle emissions. The law can quickly create the conditions for the rapid development of this market.

In the next five years, there are five areas expected to drive automotive electronics growth and technological innovation. These areas include: reducing emissions and improving engine efficiency; traditional mechanical systems transition to electronic controls (so-called "x-by-wire" systems and driver assistance systems) to increase safety and reduce power consumption; enhance personalization capabilities, Such as navigation and communication systems; the growing demand for convenience and comfort; the growing demand for cars in emerging countries.

In these five areas, navigation and communication systems and solutions to improve vehicle safety offer the greatest potential for increasing the use of semiconductors in automobiles.

Chinese auto market

The Chinese auto market is booming. According to market research firm iSupply, by 2011, China's global electronic system production will double that of semiconductor consumption, reaching $18.4 billion. The main reason for this growth is the growing demand for electronic components in domestic light vehicle production and the fact that many global automakers are shifting production activities to China.

International automotive electronics systems and component suppliers from the Americas, Europe, Japan and South Korea have started joint ventures with Chinese companies. These foreign companies include Delphi, Bridgestone and Bosch. In recent years, General Motors has invested $350 million to build a modern manufacturing facility at the Wuling joint venture headquarters in Liuzhou, Guangxi, Zhuang Autonomous Region, southwest China. These plants produce commercial, low-cost, low-fuel, light-duty vehicles. This is the opposite of GM's strategy in North America. GM sells large, expensive SUVs and trucks in North America. This strategy is currently challenged by rising gasoline prices and changes in consumer tastes. Consumers are now more and more aware of environmental protection. In addition, analysts predict that global small business demand will grow by 30% in the next decade. China's auto market grew by 25% last year. China has surpassed Japan to become the world's second largest auto market, with annual sales of 8 million vehicles. These include mini trucks and mini cars. Since China has 10% of car ownership per 100 people, and the car ownership per 100 people in the US and Western Europe is 80%, China's growth potential is huge. According to research firm AC Nielsen, China wants to own a car more than any other country, but they don't want to buy a car now. China's auto component industry will grow to $58 billion by 2009, with an average annual growth rate of 15%. China's domestic production will certainly meet the growing domestic demand for automotive components. By 2011, semiconductor consumption is expected to grow to $2.8 billion. This is nearly double the market size of nearly $1.5 billion in 2006. According to market research firm Research & Markets, this will make China the fastest growing automotive electronics market in the world. According to the report, by 2012, the average value of electronic components used in each car in China will increase from $300 in 2003 to $500.

Electronic systems and components for "four wheels"

On average, each car integrates 70 to 100 processors in 30 different functional electronic systems. These electronic systems include engine controls, drive trains, body electronics, safety, entertainment and anti-theft systems. Semiconductor equipment for automobiles includes microprocessors (usually using PowerPC and ARM architecture), 8, 16, 32-bit microcontrollers, DSP (digital signal processors), programmable logic devices, interface chips, switches, ASICs, systems Class packaged chips, memory integrated circuits, resistors, capacitors, inductors, micro-motor systems, optoelectronic components and many sensors. According to market research firm Strategy Analytics, in 2007, sensors for cars sold two 26 million units with total sales of $26 million.

In the future of automotive electronic circuits, there will be an increasing demand for accurate, closed-loop, real-time control and the requirement to process large amounts of data from multiple sensors. Systems that configure actuators (such as those used for adaptive headlights) also have a large number of semiconductor components. In particular, the micro-motor system represents a very promising technology for various automotive systems such as airbags, stability control, tire pressure monitoring, engine airflow control and occupant detection systems. Market research firm n-Stat/MDR predicts an average of at least 10 micro-motors per vehicle. The total market value of such micro-electric equipment is $1.5 billion. Other emerging applications include biosensors for remote keyless entry (PKE) systems and optical micromotor systems for multimedia displays. For example, Hitachi introduced a finger vein recognition technology last year that allows drivers to verify the driver's identity within seconds of grabbing the steering wheel. Hitachi predicts that by 2010, finger vein recognition sensors will begin to replace traditional key-based car ignition devices. With regard to virtualization solutions, the demand for larger screens and touch screens will grow. These displays include a car navigation display from 6.5 inches to 8.8 inches and a separate personal navigation device from 3.5 inches to 4.3 inches will increase to 4.8 inches to 5.2 inches.

The number of video cameras used in cars will also increase significantly. These video cameras will be used for applications such as cruise control, collision avoidance or video surveillance. Many companies, including Sharp, are developing video systems specifically for use in automobiles. Automotive video cameras will also offer WVGA resolution and will be based on CCD (for higher resolution requirements) or lower priced CMOS technology. According to market research firm Strategy Analytics, global automotive video camera shipments will reach 7 million units in 2008, and sales will reach approximately $40 million. The market associated with video cameras integrated in mobile phones will expand 50 times. However, the more stringent requirements of automotive applications will make this market a very profitable marginal market.

The use of LEDs in automobiles, especially in taillights, accounts for approximately 10% of the total market. LED-based lighting systems are known for their high efficiency, long life and low power consumption compared to incandescent systems. The popularity of LEDs in the automotive industry has been very slow so far, mainly due to the complexity of driving circuits and high production costs. At present, the production cost of LED is actively decreasing. LEDs are also ideal for lighting applications inside the car. A car needs 100 to 200 white LEDs. Therefore, the potential of this market is very large. The current size of this market is 740 million US dollars, and the compound annual growth rate is expected to be 14.2% before 2010. The growth trend of integrated circuits in automotive safety is the highest, followed by car body and car box. The growth rate is 9.8%. In these areas, accurate, closed-loop, real-time control and the requirement to process large amounts of data from multiple sensors are needed to make cars safer, more fuel efficient and more environmentally friendly.

The most important application of automotive electronics is body electronics, which had a market size of $4.4 billion in 2007, accounting for 26% of the market. In 2013, this market will reach $8 billion. The electronic system for engine control has a compound annual growth rate of 5.7% from 2007 to 2013, and the size of 2013 will increase from $5 billion in 2007 to $7 billion. This demand strongly suggests that processing power must meet increasingly stringent performance requirements. Systems that rely on view tables will shift to a model-based platform that manages large amounts of data. For example, fuel injection control is based on several factors including manifold pressure, battery voltage, engine speed, throttle position, and exhaust oxygen content. A car represents a very harsh environment for electronic equipment applications because of vibrations, temperature changes (possibly between minus 40 degrees and minus 150 degrees), fuel, and severe electromagnetic fields (up to 200V/m, while industrial And the electromagnetic field in the home is only 10V/m and 3V/m), the transient peak is ±100V peak voltage, humidity, dust, sudden load change and possible short circuit. Automotive environments require that electronic equipment must guarantee a high level of quality and reliability. A component failure can threaten the safety of the occupants of the car. Testing of automotive electronic components is carried out in accordance with the AEC-Q100 evaluation process and ISO-TS16949 technical specifications. This technical specification was developed by the International Automotive Task Force.

In the automotive information system, important task layers and convenience layers must coexist. The former controls the engine and the latter provides tools (such as electronic windows). Although the latter is not very important for security, it must always work. As the automotive industry strives to reduce failures in chip design, this will drive the need for new integrated circuit and electronic system design methods. Need a gateway. This gateway is an electronic system that acts as an interface to components such as security components, convenience layers, and telematics systems.

According to market research firm Databeans, Freescale Semiconductor is the world's leading manufacturer of automotive semiconductors, accounting for 11% of the market. Secondly, Infineon has a market share of 10%. STMicroelectronics ranked third with a market share of 9%. Renesas Technology has a market share of 7%. NEC Electronics has a market share of 6%. Other manufacturers have a market share of 58%. This shows that the automotive semiconductor market is very fragmented.

Companies operating in the automotive market are looking for ways to accelerate applications based on new semiconductors and reduce costs. These approaches include closer collaboration between system developers and semiconductor companies, industry-wide adoption of software standards, and protection of intellectual property. The use of automotive electronic systems also requires extensive experience in system level design. These experiences can be obtained through strategic cooperation. An example of such cooperation is the cooperation that began between Freescale Semiconductor and STMicroelectronics two years ago. The two companies recently launched the first four automotive power architecture microcontroller products from their joint design program.

Figure 2 Automotive electronic semiconductor devices include microprocessors that typically use PowerPC and ARM architectures.

And 8, 16, and 32-bit microcontrollers

STMicroelectronics and Mobileye, based in the Netherlands, jointly developed the EyeQ2 SoC for the automotive industry's vision-based advanced driver assistance system. In March last year, Infineon and car manufacturer Hyundai Motor Co. opened a joint technology innovation center in Seoul to jointly develop automotive electronics systems and architectures for Hyundai Motors and Kia cars, which were launched in 2010. Delphi is working with Infineon to develop a joint project. The project is based on Infineon's XC2200 series of microcontrollers and uses the Autosar standard.

Industry alliances are also key to developing adequate automotive electronics systems. These industry alliances include: OSGI (Open Services Gateway), MISRA (UK Automotive Software Reliability Association), AMI-C (American Automotive Multimedia Interface Association), ERTICO (European Road Transport Information and Communication Cooperation), which is the European Commission In order to develop its own intelligent transportation system was created in 1991. Autosar (Automotive Open System Architecture) and Jaspar (Japan Automotive Software Platform Architecture) are organizations that promote network interface standardization and enterprise application software modules. Members of the open source software Eclipse community sponsored by IBM include companies such as WindRiver, Altera, and Xilinx. The organization developed a framework that allows for the development of optimized software for the entire product lifecycle.

10.1 Inch Laptop,win10 Laptops,win11 Laptops

Jingjiang Gisen Technology Co.,Ltd , https://www.jsgisengroup.com